Are Global Trade Rules Pushing Small Businesses Out?

- News Desk

- Dec 23, 2025

- 7 min read

The proposal put forth by the European Commission (EC) to revise statistical rules that govern the recording of International Trade in Services (ITS), Balance of Payments (BOP), and Direct investment abroad would provide an opportunity for the Global South to participate more fully in developing the global economy, especially in light of the Indian government's goal of reaching a $5 trillion economy.

India is not only the world's largest recipient of remittances, but it is also becoming a centre for information technology (IT) and business process outsourcing (BPO), which means that these proposed amendments will not just change the way in which India will report the economic value they generate, but also how the international community views Indian economic activity. Ascertainment of an International Standard (such as the International Monetary Fund's Balance of Payments Manual, sixth edition or BPM6) is required for India to compete globally; however, the current proposal may impose an excessive compliance cost on small and medium enterprises (SMEs) and put them in direct conflict with India's new Data Sovereignty framework. This feedback is based on the experience of Indian public sector organisations, private enterprises and digital labour.

The economic landscape of India, as compared to the European single market, is very different. To illustrate, the Indian service sector consists of many different disconnected elements, with the majority of Indian services being exported by way of start-ups, freelancers and Micro, Small and Medium Enterprises (MSMEs), versus large conglomerates. Additionally, India occupies a pivotal position within the global supply chain, and likewise, provides intangible value (including software code, research and development (R&D), business processes) to the worldwide economy, due to the nature of these activities, poses a major challenge when doing trade statistics.

If the proposed changes establish a rigid method of collecting data as dictated by advanced economies, as a result the small and medium-sized enterprises in India will not be included in the formal statistical markets or worse, European businesses will refrain from trading with Indian vendors due to the cumbersome nature of the data collection process and the requirements for compliance.

The burden of compliance for Indian SMEs/Startups: the proposed requirements for the collection of granular level information such as Ultimate Beneficial Owner (UBO) and more specified service trade breakdowns would be a significant challenge for Indian Micro, Small and Medium-sized Enterprises (MSMEs), as opposed to the majority of European businesses, many of which utilize integrated digital accounting systems that are fully supported by Eurostat standards, many Indian exporters operate with a wide variety of administrative structures.

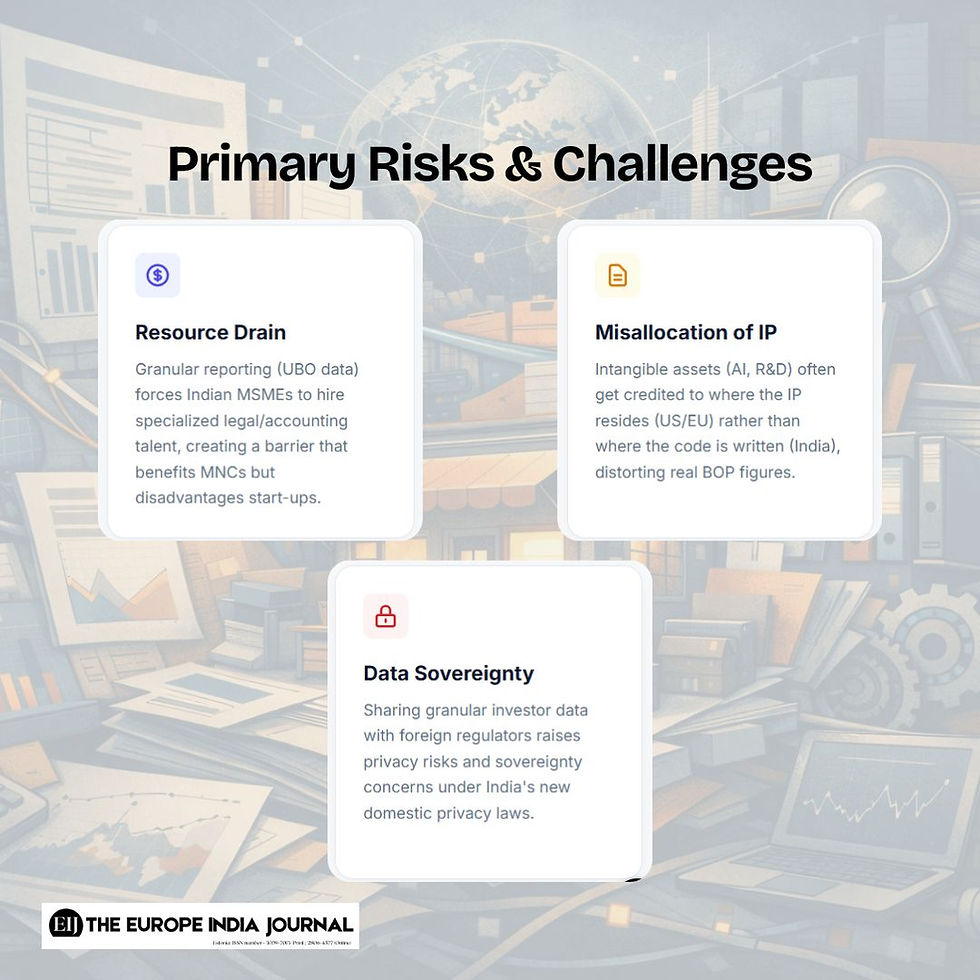

Resource Drain: To maintain the level of granularity suggested for tracking and reporting data at mid-sized Indian IT companies, they need to hire additional specialized legal & accounting resources, leading to an increased cost barrier, which could place mid-sized Indian companies at a distinct disadvantage to larger global corporations (MNCs) that can absorb these costs associated with compliance.

Risk of Exclusion From The Market: The concern exists that if the reporting burden is too high, then within the European Market, European Importers will consolidate their supply chains and only work with the larger established incumbents in India (TCS or Infosys) that can more readily provide the necessary statistical data and leave out all the start-ups in the vibrant Indian start-up ecosystem.

India's Digital Economy continues to develop rapidly, often blurring the lines between Goods and Services. Current statistical provisions don't always have the ability to measure cross-border supply as accurately with "Mode 1" services, where India is a strong leader.

Intangible Assets: Much of the value of India's exports is derived from intangible assets, specifically proprietary algorithms, AI models, and R&D (Research & Development). Without the new guidelines being clearly defined and made flexible in their approach to valuing intangible assets, more often than not, the economic output that originates in India will be incorrectly allocated to the country where the intellectual property (IP) resides, generally either the United States or the European Union. The misallocation of this economic productivity prevents India from receiving appropriate credit for it in balance of payments (BOP) statistics.

"Ultimate Beneficial Owner": While India continues to attract large amounts of foreign direct investment (FDI) (more than $70 billion annually; Department for Promotion of Industry and Internal Trade), capital flows through various countries/jurisdictions as FDI so that they can use efficient tax strategies by using these intermediate jurisdictions such as Singapore or Mauritius. Even though the proposed changes would require the reporting country to report the ultimate investing country (UIC) in India (and will increase transparency around FDI into India), the complexities inherent in identifying the UBO (ultimate beneficial owner) in multi-layered transactions and the logistical nightmare for Indian regulators and businesses make it impractical to implement.

The Reserve Bank of India (RBI) has existing reporting standards that are stringent and will now require an additional set of reporting standards for European Investments, resulting in a possible dual compliance challenge for Indian companies and could have an effect on the level of desire for European Investments.

Cross-border Data Sharing: These amendments also require greater sharing of Data between National Statistical Authorities so that they can complete their mutual data flows. India has concerns over sharing granular and detailed data on its Investors or Service suppliers with an entity or entities outside of India due to a question of sovereignty.

Privacy Risks: The Requirement to identify Ultimate Ownership means processing Personal Data in India. There are concerns among Indian stakeholders, that without specific “Safe Harbour” provisions, compliance with these Statistical Reporting Requirements will either place them in violation of Indian Domestic Privacy Laws or place commercially sensitive strategy in the hands of foreign regulators (European Parliament & Council of the European Union 2016).

RECOMMENDATIONS FROM AN INDIAN FRAMEWORK

In order for the amended statistical provisions to create a truly inclusive global economy that does not put undue burden on the developing economies of partner countries (such as India), we recommend:

The European Commission should promote the idea of a ‘Proportionality Principle’ regarding international reporting. A separate tier of less complicated reporting should be created for SMEs and developing countries. This would enable Indian MSMEs to take part in and contribute to the European supply chain without facing the same robust unqualified reporting requirements as global multinationals.

Build Capacity and Transfer Technology

The EU should collaborate with Indian agencies such as Directorate General of Commercial Intelligence and Statistics (DGCI&S) and Reserve Bank of India (RBI) to build the necessary digital infrastructure to support new International Reporting. This includes funding capacity building workshops and providing access to software used by Eurostat. In turn, this would enable Indian agencies to collect this data in a timely and accurate manner (International Monetary Fund, 2021).

Update Definitions of Services Trade

Definitions related to Services Trade will be updated to clearly define and include Gig Work performed through platforms such as Uber, TaskRabbit, Upwork and other similar services. The European Union and India must form an international working group to identify methods for aggregating and anonymizing data collected from Digital Platforms, such as Upwork, to provide a data-driven estimate of contribution of Independent Contractors (freelancers) in India to the economies of EU nations. (OECD, 2023)

Data Law Harmonization with India

Developing a clear protocol for ensuring that all Data shared for Statistical purposes complies with India’s Digital Personal Data Protection Act (PDPP A). Protocols must ensure that "Ultimate Beneficial Owner" data is required to be anonymized before leaving the jurisdiction of India so that anonymized data can be shared in compliance with statistical transparency requirements without compromising the individual Privacy of Data subjects and India’s sovereignty over its Data.

Phase Implementing Attribution of Foreign Direct Investment (FDI)

Recognizing the challenges associated with Global Financial Structures, providing India a phased implementation of reporting Ultimate Investing Countries, over a period of five to seven years, would be beneficial for India. This timeframe allows the Corporate Ecosystem of India to adjust its compliance structures and permits the Government of India to upgrade the "Foreign Investment Facilitation Portal" to include digital means of capturing this data while maintaining the existing flow of foreign direct investment (FDI) into India (European Commission, 2022).

The compliance of India with the objective of transparent and robust global statistical economic data includes their intention to provide for a new model of global statistical economic data that addresses the realities and "digital divide" faced by many of those who are part of the Global South, including but not limited to India itself. Accurate statistical data is critical to the economic health and success of India, but would not be achieved if SMEs were denied market access and/or if data sovereignty were compromised.

A more flexible and capacity-aware approach by the EU to create statistics that not only address current needs of businesses to conduct trade in an emerging economic environment and to be able to participate in a rapidly changing economic environment, but that also accurately depict and develop the deepening economic relationship between India and Europe instead of erecting new barriers to trade and market entry, will ultimately produce an accurate and effective use of current statutory European Economic Area laws.

This article is written by

Prarabdh Seth, EICBI Public Policy and International Affairs Intern

REFERENCES

European Commission. (2022). Second annual report on the screening of foreign direct investments into the Union(COM(2022) 433 final). https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:52022DC0433

European Commission. (2024). Commission Delegated Regulation (EU) 2024/3104 of 2 September 2024 amending Regulation (EC) No 184/2005 of the European Parliament and of the Council, as regards references to the statistical classification of economic activities NACE established by Regulation (EC) No 1893/2006 of the European Parliament and of the Council. Official Journal of the European Union, L, 2024/3104. https://eur-lex.europa.eu/eli/reg_del/2024/3104/oj/eng

European Parliament & Council of the European Union. (2016). Regulation (EU) 2016/679 of the European Parliament and of the Council of 27 April 2016 on the protection of natural persons with regard to the processing of personal data and on the free movement of such data, and repealing Directive 95/46/EC (General Data Protection Regulation). Official Journal of the European Union, L 119, 1–88. https://eur-lex.europa.eu/eli/reg/2016/679/oj

Eurostat. (2023). European business statistics geonomenclature applicable to European statistics on international trade in goods – 2023 edition. Publications Office of the European Union. https://ec.europa.eu/eurostat/web/products-manuals-and-guidelines/w/ks-gq-23-009

International Monetary Fund. (2021). IMF annual report 2021: Build forward better.https://www.imf.org/external/pubs/ft/ar/2021/eng/downloads/imf-annual-report-2021.pdf

International Monetary Fund. (n.d.). Guidance note C.3: International trade classified by currency (including for trade linked to long-term trade credits and advances). https://www.imf.org/-/media/files/data/statistics/bpm6/catt/c3-international-trade-classified-by-currency.pdf

OECD, WTO, IMF, & UNCTAD. (2023). Handbook on measuring digital trade (2nd ed.). OECD Publishing. https://www.oecd.org/content/dam/oecd/en/publications/reports/2023/07/handbook-on-measuring-digital-trade-second-edition_099afd2f/ac99e6d3-en.pdf

United Nations Conference on Trade and Development. (2024). World investment report 2024: Investment facilitation and digital government. United Nations. https://unctad.org/publication/world-investment-report-2024

World Trade Organization. (2023). World Trade Statistical Review 2023.https://www.wto.org/english/res_e/booksp_e/wtsr_2023_e.pdf

Comments